The stock market is not fair.

The billion dollar players have rigged the game so regular folks do not have a fair chance.

That leaves us with a simple choice:

Keep losing to them or...

Get on the same side of the game with them.

Us? We'd rather be on the winning side with them.

Wouldn't you?

You'll see why you've been losing this rigged game and how to get on the winning side.

Talk soon,

Shawn Casey & Brian Koz

Why eBay's Depop Acquisition Matters More Than the Earnings Beat

Reported by Chris Markoch. Originally Published: 2/20/2026.

Key Points

- eBay’s Q4 beat and GMV acceleration support a comeback narrative, even as the stock remains pressured by broader “AI trade” sentiment.

- Advertising and recommerce are emerging as durable growth engines, while Depop adds a targeted Gen Z/Millennial wedge.

- Depop integration costs, cyclical category tailwinds, and margin pressure remain the main risks to watch.

- Special Report: [Sponsorship-Ad-6-Format3]

Shares of eBay Inc. (NASDAQ: EBAY) are about 3.8% higher the day after the company delivered a strong Q4 2025 earnings report. On the surface, the results make sense: eBay is a pure play on consumer spending, which has remained resilient despite mixed macroeconomic data. And eBay fits into the "discount" category of retail stocks that have held up well in a volatile market.

There was a lot for investors to like. Revenue of $2.97 billion topped expectations of $2.87 billion. A key metric, gross merchandise volume (GMV), climbed to $21.2 billion—up almost 6% globally and nearly 10% in the United States—suggesting the platform is growing and attracting more customers.

My blood is boiling… and yours should be too (Ad)

Fraud is being exposed everywhere right now. Billions gone.

But they're missing the big one...

A legal scam that affects 95% of ALL Americans.

Oxford Club's own Marc Lichtenfeld hit the streets of South Florida to expose it in broad daylight.

Watch along as he captures real people's reactions LIVE on camera.

Another headline from the quarter was the announcement that eBay will acquire Depop, the secondhand clothing marketplace owned by Etsy Inc. (NASDAQ: ETSY), for $1.2 billion in cash. The deal is a strategic move to capture more Gen Z and Millennial customers.

Like many stocks with even minimal exposure to artificial intelligence (AI), EBAY traded lower in 2026 ahead of the report. One solid quarter won't erase that trend, but there are several reasons to believe in eBay's comeback.

Ads, Fashion, and the Recommerce Angle

The Q4 report highlighted three growth engines. First, advertising: on an annualized basis, eBay is approaching $2 billion in ad revenue, a stream that was almost non-existent five years ago.

Total advertising revenue was $544 million in Q4, implying GMV penetration of nearly 2.6%, with first‑party ads growing more than 17% to $517 million. About 4.8 million sellers adopted at least one promoted-listing product during the quarter. The takeaway is that advertising is becoming embedded behavior on the platform, not just an optional feature for power sellers.

The second engine is recommerce (pre‑owned and refurbished merchandise). That category accounted for more than 40% of eBay's GMV in 2025 and grew about 10% during the year. This is an area where eBay is differentiated from Amazon.com Inc. (NASDAQ: AMZN), and one Amazon will be hard‑pressed to replicate at scale.

The third—and potentially highest‑upside—engine is the Depop acquisition. In 2025, Depop generated roughly $1 billion in gross merchandise sales for Etsy. Crucially, nearly 90% of Depop's 7 million active buyers are under 34, a demographic eBay has struggled to attract.

Depop also specializes in fast‑growing fashion segments. If those shoppers migrate to eBay, the platform could gain a credible foothold in categories that drive higher engagement and revenue growth.

A Marketplace Revamp With Real Teeth—or Temporary Tailwinds?

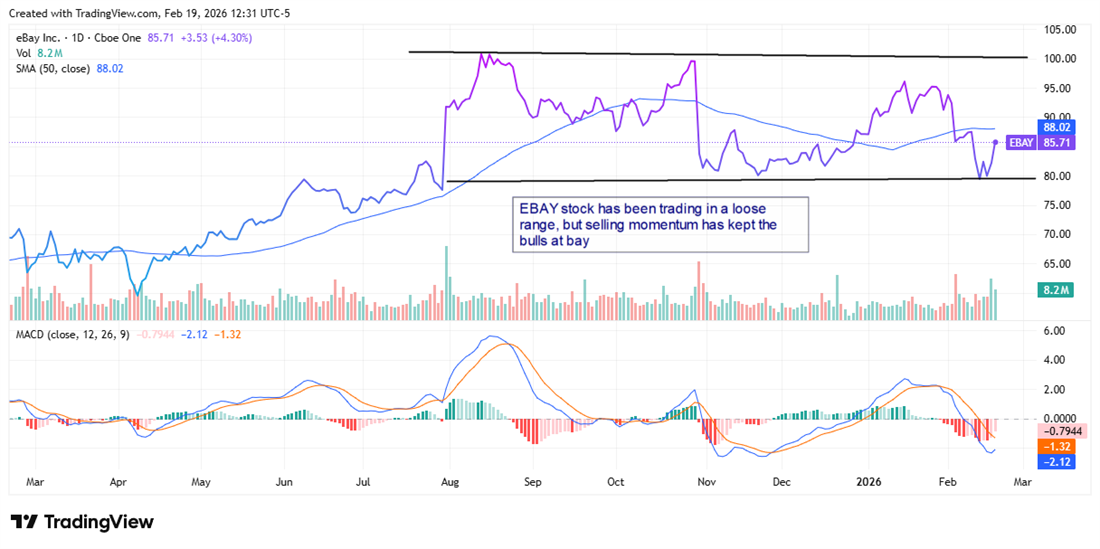

Institutional sentiment toward EBAY has been bearish over the last three quarters, with net selling exceeding buying by about $2 billion. Some of that selling followed the stock's run to an all‑time high in August 2025. Since then, EBAY has traded in a loose range with support near $80 and resistance around $100.

Analyst coverage on MarketBeat shows that many firms have already raised price targets on EBAY. Several new targets exceed the consensus price target of $96.52—about a 12% premium to the current share price at the time of writing. The most bullish among them is Needham & Company, which nudged its target up to $122 from $115.

Investors should also consider the company's dividend. A dividend alone isn't a reason to buy a growth‑oriented name like eBay—investors should want to see continued investment in growth, such as the Depop deal.

That said, the dividend yield of 1.35% is above the S&P 500 average. eBay has raised its payout at an average annual rate of more than 14% over the past three years; the current annual dividend is $1.16. The payout ratio is just over 25%, which appears sustainable and not a strain on cash flow.

Risks That Investors Shouldn't Ignore

The bull case is compelling, but there are several risks to keep in mind. First, some of Q4's GMV growth was commodity‑driven. Management noted on the earnings call that bullion, collectible coins, and Pokémon trading cards provided meaningful tailwinds in late 2025—categories that are inherently cyclical and unlikely to recur at the same pace.

Second, the Depop acquisition, while strategically sensible, carries near‑term costs. eBay expects the deal to be a low single‑digit headwind to non‑GAAP operating income growth and to dilute EPS in the short term; accretion is not expected until 2028.

Third, non‑GAAP gross margin slipped nearly 80 basis points year over year. Sustainable margin expansion in the face of Amazon's logistics network and Shopify's (NASDAQ: SHOP) seller ecosystem remains the central question weighing on EBAY. Management says the margin pressure was primarily driven by scaling managed shipping and Authenticity Guarantee programs—necessary investments that underscore the real costs of maintaining trust on a peer‑to‑peer marketplace.

Berkshire & AI Hyperscalers: Buffett Holds GOOGL, Dumps AMZN

Reported by Leo Miller. Originally Published: 2/18/2026.

Key Points

- Berkshire Hathaway's latest 13F filing revealed interesting moves from Q4 2025, especially regarding AI hyperscalers.

- The company initiated a position in a top media company, pushing hard into the digital economy.

- While Berkshire sold a portion of its AAPL holdings, the Magnificent Seven stock remains its largest position.

- Special Report: [Sponsorship-Ad-6-Format3]

Investment giant Berkshire Hathaway (NYSE: BRK.B) just released its Q4 2025 portfolio moves. The company’s 13F filing details the trades it made during the quarter ending Dec. 31, providing insight into its views on several notable names. The firm’s key portfolio changes include one of the world’s most well-known media companies and multiple Magnificent Seven stocks.

This latest round of trades is particularly noteworthy. At the end of 2025, Berkshire founder Warren Buffett retired as CEO. Greg Abel has since taken over the role, while Buffett remains Chairman of the Board and continues to exert significant influence.

My blood is boiling… and yours should be too (Ad)

Fraud is being exposed everywhere right now. Billions gone.

But they're missing the big one...

A legal scam that affects 95% of ALL Americans.

Oxford Club's own Marc Lichtenfeld hit the streets of South Florida to expose it in broad daylight.

Watch along as he captures real people's reactions LIVE on camera.

These were therefore Berkshire’s final portfolio moves while Buffett occupied the CEO role. As he steps back after an extraordinary 60-year run, here are the most significant trades from Q4 2025.

The New York Times: Berkshire’s Shiny New Holding

In Q4, Berkshire initiated a new position in New York Times (NYSE: NYT), buying nearly 5.1 million shares — a relatively small stake given the size of Berkshire’s overall portfolio.

At the end of Q4, that position was worth roughly $352 million, or about 0.13% of Berkshire’s equity holdings.

NYT shares performed well in Q4, rising roughly 21%, and have continued to climb in 2026. NYT’s November earnings report was a catalyst for the rally.

In that quarter, the company added 460,000 net new digital subscribers, a 77% year-over-year increase. Digital advertising revenue rose 20% that quarter and accelerated to 25% in NYT’s latest earnings.

Berkshire’s purchase signals confidence in NYT’s ongoing digital transformation.

Berkshire Reduces Apple Stake, Trims Several Key Names

Notably, Berkshire trimmed its stake in Apple (NASDAQ: AAPL) by 4% during Q4, continuing a recent trend of modest sales. In Q2 2025 it cut Apple holdings by about 7%, and reduced them by 15% in Q3 2025.

Despite the reductions, Apple remained Berkshire’s largest position, valued at nearly $62 billion at the end of Q4 — roughly 23% of the equity portfolio — indicating continued long-term conviction in the iPhone maker.

Other notable reductions included selling about 48% of its stake in the Atlanta Braves (NASDAQ: BATRK), a 9% cut in Bank of America (NYSE: BAC), and a 3% reduction in Constellation Brands (NYSE: STZ). The biggest headline, however, was Berkshire’s sale of hyperscaler and Magnificent Seven giant Amazon.com (NASDAQ: AMZN).

AMZN vs GOOGL: Berkshire Dumps One, Holds the Other Steady

During the quarter, Berkshire sold more than 7.7 million Amazon shares, trimming its holdings from about 10 million shares to roughly 2.3 million — a 77% reduction. The sale was abrupt compared with prior activity; Berkshire hadn’t meaningfully reduced AMZN since lowering holdings from 11 million to 10 million in Q3 2023.

The rationale is open to interpretation, but Amazon reached an all-time closing high of $254 in Q4 and has since fallen roughly 20%. That peak may have prompted Berkshire to pare back.

Berkshire may also have anticipated Amazon’s aggressive capital expenditure (CapEx) guidance: the company plans roughly $200 billion in CapEx for 2026 — the highest among hyperscalers and about $50 billion above analyst expectations, according to S&P Global.

Amazon’s CapEx outlook was a significant pressure point after its recent earnings report.

By contrast, Berkshire left its position in Amazon’s cloud rival, Alphabet (parent of Google, NASDAQ: GOOGL), unchanged. Alphabet also hit multiple all-time highs in Q4, and Berkshire’s decision to hold suggests greater confidence in Google’s cloud and AI strategy relative to Amazon’s.

Analyst Forecasts Clash with Berkshire’s Long-Term Perspective

One of the more interesting takeaways is not just what Berkshire sold, but what it chose to keep. Selling much of AMZN while maintaining GOOGL indicates a clear preference for Alphabet.

Analyst price targets, however, tell a different short-term story: the consensus target on AMZN implies roughly 43% upside, while the consensus target on GOOGL implies about 20% upside. Keep in mind those targets are 12-month forecasts; Berkshire typically takes a multi-year view, and its trades likely reflect where it sees long-term value.

This email communication is a sponsored email sent on behalf of Trade Canary, a third-party advertiser of The Early Bird and MarketBeat.

If you have questions about your subscription, please email MarketBeat's South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from The Early Bird, you can unsubscribe.

Copyright 2006-2026 MarketBeat Media, LLC. All rights protected.

345 N Reid Pl., Sixth Floor, Sioux Falls, South Dakota 57103-7078. USA..