Why I'm avoiding Nvidia (and buying these 3 AI stocks instead) (From TradingTips)

Oracle Speaks! The Message: AI Demand Outpaces Capacity Written by Thomas Hughes on March 11, 2026

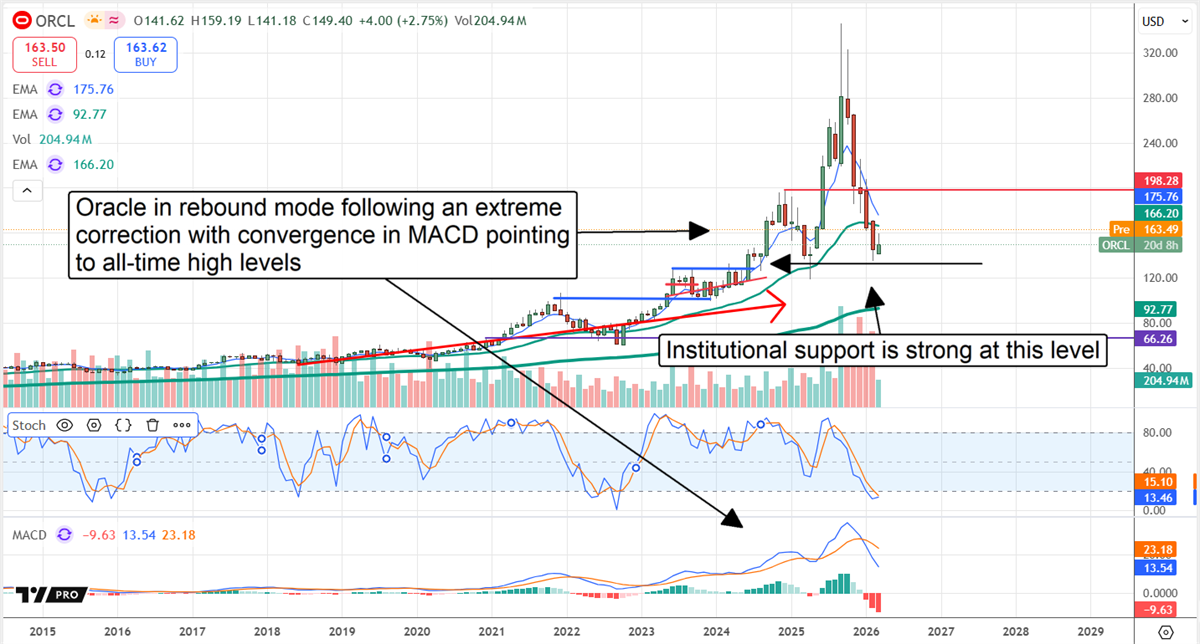

Key Points - Oracle's Q3 release affirms its robust outlook and upped the ante with improved long-term guidance, and the analysts liked it.

- Price target increases and upgrades point to rising share prices and the potential for a robust rebound and fresh all-time highs.

- Institutions accumulated in Q1 when prices were low, providing a support base and limiting risk in 2026.

- Special Report: Every morning, an AI ranks 357 stocks for you (From TradingTips)

Oracle’s (NYSE: ORCL) stock price could be poised to experience the hottest upswing in modern tech history. The company’s fiscal Q3 2026 release not only affirmed the robust outlook and allayed debt-related fears, but also upped the ante by improving forward guidance. The takeaway for investors is that, to use the words of JPMorgan (NYSE: JPM) analysts (who upgraded the stock), the news provides the clearest proof yet that the company’s AI strategy is working. Oracle is emerging as a powerhouse of AI innovation, providing not only the infrastructure to support it but also the tools to develop it and applications derived from it, all while delivering ever-improving services to legacy and new clients. Warren Buffett is the greatest value investor of all time. But even the Oracle of Omaha has limits.

Because of Berkshire Hathaway's size, Buffett simply can't invest in small-cap stocks without taking controlling stakes. That means some of the market's most promising companies are completely off his radar.

But they don't have to be off yours.

We've put together a brand-new report profiling 5 small-cap stocks that check all the boxes of Buffett's investing criteria solid financials, durable business models, strong management, and clear growth catalysts.

The only difference?

These stocks are flying under Wall Street's radar and still accessible to individual investors like you. >> Click here to get your free copy of this report Analysts, Institutional Buying, and Price Action Align: Robust Rebound Brewing Analysts are responding as expected—either reaffirming already bullish outlooks, issuing upgrades, or raising price targets. Sentiment has shifted back to an aggressively bullish posture, reversing the trend of price target reductions, strengthening the Strong Buy rating, and improving the rebound outlook. As it stands, the bias is firmly bullish, with 75% of the ratings pegged at Buy or higher equivalents, the single Sell rating is more than a year old, and the price target offers an 80% upside from the pre-release closing price, with trends pointing to the high-end range. The high-end is pegged at $400, more than 165% upside, and may be reached well before the year’s end. Institutional trends align with a bottom in price action and an outlook for sustained upward momentum in the stock price. While this group sold on balance in Q4 2025, the bearish behavior ended with the turn of the New Year as they reverted to accumulation. The balance of activity in early Q1 is more than $1.50 bought for each $1 sold, providing a tailwind for this market, which is likely to strengthen as the year progresses. And the charts. The charts are set up for a bullish momentum swing, with indications on the daily, weekly, and monthly price charts that the market is deeply oversold. The likely outcome is that this market retests its all-time high, with the potential to exceed it by $140 to 100%. The $140 upside is also a base case scenario, derived from the magnitude of Oracle’s recent pullback, assuming fresh highs are set. In this case, a break to new highs signals a trend continuation, leading to another move ranging from the prior move’s dollar value to the percentage gain it represents: $140 or 100%.

Oracle Rebounds on Outperformance and Acceleration Oracle had the hottest quarter in over 15 years in Q3. Its revenue grew more than 21% to $17.19 billion, accelerating sequentially and year over year (YOY), outpacing the consensus by 165 basis points. The strength was driven by gains across the board, led by a 44% increase in total cloud revenue. Total cloud grew by 44% to nearly $9 billion, accounting for nearly 52% of the revenue. Cloud infrastructure grew by 84%, underpinned by a 531% increase in Multi-Cloud Database and 243% gain in AI infrastructure. SaaS grew by 13%, with gains in Fusion and NetSuite driving it. Margin news was also strong. The company leveraged its revenue strength, outpacing consensus earnings estimates across all levels despite increased spending and a higher debt load. The bottom line is $1.70 in adjusted earnings outpaced consensus by 590 basis points, driving significant cash flow, and the strength is expected to continue. Guidance will drive this market higher now that the rebound is underway. The company issued hot guidance for Q4, implying better-than-forecast full-year results, and raised its outlook for the subsequent year. Oracle now expects revenue growth to accelerate to over 31% annually, outpacing estimates for revenue and earnings by wide margins. Among the drivers will be the rapid expansion of cloud and AI capacity, with at least another 14 or 25% hyperscaler instances coming online in the near future. 7 High Yield Dividend Stocks to Buy Now 💰

Love steady payouts? This free report reveals 7 high-yield dividend stocks you need to know about. From Company #3, a tobacco giant innovating with smokeless products, to Company #4, famously known as "The Monthly Dividend Company," these picks deliver steady income you can count on. Perfect for income-focused investors. Oracle’s Debt, It’s Not a Concern So Much as a Need Oracle’s debt and share count are growing to support its growing AI network. While concerns about debt are valid, they are offset by the need for financing. The Q3 results and swelling backlog, now at $553 million, up 325% YOY, suggest rapid expansion is needed; otherwise, another business will do it first. The critical detail for investors is that the backlog remains more than 4.4 times the debt, equivalent to approximately 8 years of business at the Q3 pace, and will be recognized much quicker. This will enable rapid debt reduction and a rapidly swelling shareholder equity in the coming years. Risks include the need for additional capital, but these will be mitigated if the backlog continues to grow. Read this article online › Featured Stories

Did you learn something from this article?

|