Editor's Note: Please read the following note from 60-year Wall Street legend Marc Chaikin,who recently held an emergency broadcast at 4 World Trade Center to share a shocking development at an AI lab Time magazine calls "the most disruptive company in the world."

Dear Reader,

This rapidly growing AI lab has been having an incredible year.

The U.S. military used its technology to capture Venezuelan President Nicolas Maduro...

NASA harnessed it to plot a rover mission – 140 million miles away on Mars...

Goldman Sachs set it to work on its most complex back-office operations...

Even rival Mark Zuckerberg is trusting it to help him run Meta Platforms!

But this is just the beginning.

I recently reviewed a leaked 512,000-line source code that exposed their new breakthrough, Project Tengu...

And what I found is truly shocking.

Click here to see the full story because...

According to the Guardian, this could "upend the entire US economy, from jobs to markets and mortgages."

Regards,

Marc Chaikin

Founder, Chaikin Analytics

P.S. This lab has grown its sales 10-fold every year since it was founded just three years ago. In fact, its annualized revenues recently surpassed both OpenAI and SpaceX. But based on my findings, it’s only scratching the surface of its true moneymaking potential. This could be extremely lucrative for early investors – but you have to move quickly. This growth story could accelerate dramatically as early as June 16. Click here to learn more...

Microsoft Is Spending Billions on AI, But Investors Aren’t Buying It

Reported by Chris Markoch. Published: 5/28/2026.

Key Points

- Microsoft is investing heavily in AI infrastructure through a massive multiyear CapEx cycle.

- Azure AI revenue growth is accelerating, but investors remain focused on profitability and returns.

- Microsoft Build 2026 could provide important catalysts tied to enterprise AI adoption and Copilot monetization.

- Special Report: Elon Musk’s $1 Quadrillion AI IPO

Microsoft Corp. (NASDAQ: MSFT) delivered what, by almost any conventional measure, was a spectacular quarter.

Revenue climbed, cloud growth reaccelerated, and Azure posted numbers that beat even the most optimistic analyst models.

The #1 stock to buy BEFORE the June 12th filing (Ad)

When the SpaceX IPO launches, most retail investors will be locked out. The banks, funds, and insiders get in early - while everyone else waits on the sidelines.

But one small infrastructure supplier - a critical piece Musk can't scale the Colossus network without - is still trading well under institutional radar. A new briefing reveals the name and ticker at no cost.

Get the SpaceX infrastructure stock name and ticker hereOn paper, this is a company firing on all cylinders. And yet MSFT shares have shed roughly 15% in 2026, underperforming the broader market at a time when artificial intelligence is supposed to be the defining tailwind of the decade.

The disconnect reflects a fundamental tension at the heart of the Microsoft investment case: the gap between what the company is building and when that build-out is expected to start paying back shareholders.

A $190 Billion Conviction Trade

It’s important to consider counterarguments when investing in any stock. In Microsoft’s case, one of the more compelling arguments centers on capital expenditure (CapEx). Microsoft has committed to spending $190 billion in capital expenditure over the coming years to construct the data center infrastructure it believes will underpin the AI economy.

CEO Satya Nadella has framed this as a once-in-a-generation infrastructure moment—comparable, in Microsoft's telling, to the buildout of the electricity grid or the early internet backbone. The argument is that whoever controls AI compute at scale in 2026 will extract disproportionate value for the next decade. Walk away from the CapEx now, the logic runs, and you hand the advantage to Amazon (NASDAQ: AMZN), Alphabet (NASDAQ: GOOGL) or a wave of well-funded challengers.

The company has plenty of cash, ending its most recent quarter with $78 billion in cash and $15.8 billion in free cash flow. Still, $10 billion here and $10 billion there quickly adds up to real money. $190 billion is larger than the GDP of many nations. It dwarfs the CapEx cycles of the prior cloud era. And it runs the risk of compressing margins and consuming free cash flow precisely when investors are scrutinizing every dollar of return.

That’s why Microsoft is likely turning to the capital markets for financing. Adding debt to the balance sheet isn’t the issue. But the cost of that financing could be for two reasons.

First, although Microsoft is monetizing AI, it’s not yet doing so at a scale that’s reassuring investors. Second, if inflation remains sticky, the Federal Reserve is not likely to lower rates. Interest rates aren’t punitive on a historic basis, but companies are financing at significantly higher rates than they were just a few years ago.

That said, analysts from HSBC and Morgan Stanley have been taking the other side of that view. In Q3 of its fiscal year 2026, Microsoft generated an annual revenue run rate of over $37 billion. That was up 123% year-over-year. Both firms are modeling for significantly higher AI revenue, which the market may not be fully pricing in.

Microsoft Build 2026: Wall Street Will Be Watching

Scheduled for June 2–3, 2026, Microsoft Build is the company's flagship annual event for developers and enterprise customers. In recent years, Build has served as a product showcase for the developer community and a de facto investor day for anyone trying to read the state of Microsoft's AI ambitions.

This year, the stakes are unusually high. After a year of aggressive product announcements, Build 2026 is where Microsoft needs to put all of that together. The key questions the market will be asking: Are enterprise customers actually deploying these tools at scale? Is Azure AI revenue becoming a structurally larger portion of cloud revenue? And what does the agent economy look like in practice?

Catalysts from Build could include meaningful announcements on Copilot monetization, new Azure AI capacity commitments, expanded details on OpenAI integration, or partnerships that signal that enterprise adoption is accelerating. A weak showing—or a conference that feels more aspirational than operational—risks extending the stock's year-to-date underperformance.

Microsoft is Miscast In the AI Revolution

The chart for MSFT hasn’t changed much in the last few months. On the positive side, it looks like the lows are in. But the stock didn’t get a lift after earnings, which stalled the rally. Now it’s forming what could be a bull flag pattern, but that requires confirmation.

What’s clear is that MSFT isn’t doing much of anything, which traders find frustrating when other AI names are surging. But if investors are expecting Microsoft to behave like a speculative stock, they’re going to be disappointed. This is a stock that investors buy and hold, letting time do its work.

Patience is required, but investors have seen pullbacks in MSFT in the past five years. Each one has been an opportunity to accumulate as the stock has made a higher high. The consensus price target for MSFT is right around $560. That marked the all-time high in October 2025. Wedbush comes in at $575, and other analysts have price targets higher than that.

That optimism is based on what the company is showing in AI revenue right now, and what that will mean for the future. It’s a story that won’t end when a data center is built, which means MSFT is a story that’s still in the early stages.

3 Stocks Rallying on Micron's Price Boost: Substance or Hype?

Reported by Dan Schmidt. Published: 5/28/2026.

Key Points

- UBS raised its Micron price target to $1,625 on May 26, citing long-term AI hyperscaler agreements and a concentrated three-company HBM supply chain.

- Western Digital and Rambus rallied in sympathy with Micron and appear fundamentally supported by similar data center demand and supply dynamics.

- onsemi's 9% sympathy rally looks unwarranted, as automotive chips dominate its revenue and the stock appears technically overextended after an 80% three-month gain.

- Special Report: Elon Musk’s $1 Quadrillion AI IPO

The raging semiconductor rally got another boost this week when UBS analyst Timothy Arcuri raised his price target on Micron Technology Inc. (NASDAQ: MU) to a stunning $1,625, nearly triple his previous target.

At the time of the upgrade, the stock was trading below $800, so the new target implied more than 100% upside and a company valuation of over $1.8 trillion.

The #1 stock to buy BEFORE the June 12th filing (Ad)

When the SpaceX IPO launches, most retail investors will be locked out. The banks, funds, and insiders get in early - while everyone else waits on the sidelines.

But one small infrastructure supplier - a critical piece Musk can't scale the Colossus network without - is still trading well under institutional radar. A new briefing reveals the name and ticker at no cost.

Get the SpaceX infrastructure stock name and ticker hereMU shares rallied nearly 20% the following day, and the entire industry seemed to join in, as the iShares PHLX Semiconductor ETF (NASDAQ: SOXX) rose 6%.

When the entire industry seems to rally every day, it's easy for undeserving companies to get caught up in the wave and soar to new all-time highs. But it's also crucial to remember Warren Buffett's quote about what happens when the wave recedes: you find out who’s been swimming without proper attire.

Why UBS Boosted Its MU Price Target by 200%

Arcuri’s May 26 MU price target increase reflected his view that high-bandwidth memory (HBM) is undergoing a fundamental shift from a cyclical semiconductor business to one driven by long-term AI infrastructure demand.

Instead of a cyclical manufacturing industry, HBM now has structural growth tailwinds led by two key factors:

Long-term Revenue Visibility: AI hyperscalers are running into HBM backlogs and are more willing to lock in long-term agreements for supply and access to next-gen products. Micron already has agreements in place for its entire 2026 HBM supply.

Concentrated Supply Chain: Producing HBM products at large scale is a capability currently held by only three companies: Micron, Samsung Electronics Ltd. (OTCMKTS: SSNLF), and SK Hynix. In its Q1 2026 earnings report, Micron projects that data center demand for HBM will exceed $100 billion by 2028, more than three times the $35 billion in HBM sales to data centers in 2025.

Given these secure, long-term agreements and heavy supply concentration, Arcuri argues that MU shares deserve a valuation similar to NVIDIA Corp. (NASDAQ: NVDA). However, the stock traded at under 10x forward earnings at the time of the call—far cheaper than the NASDAQ 100 average of 24x earnings—hence the massive re-rating.

3 Stocks Rallying in Sympathy: Hype or Substance?

Many tech stocks in the AI and semiconductor space rallied hard in sympathy, especially Western Digital Corp. (NASDAQ: WDC), Rambus Inc. (NASDAQ: RMBS), and onsemi (NASDAQ: ON). But are these gains warranted? Despite the industry's exuberance, each company still requires substantial due diligence to separate substance from hype.

Western Digital: A Clean Complement to Micron’s Surge

Western Digital Corp. also rallied 8% on the day of the report, bringing its total year-to-date (YTD) gain to over 200%.

Western Digital is now a pure hard disk drive (HDD) manufacturer following the SanDisk spinoff, and the same logic UBS applied to Micron’s HBM products also applies to Western Digital’s HDDs.

Hyperscalers are locking in long-term agreements, and the company’s production capacity throughout 2026 has already been claimed. The fiscal Q3 2026 earnings report on April 30 confirmed the bull thesis with a massive double beat featuring 45% year-over-year (YOY) revenue growth and gross margins above 50%.

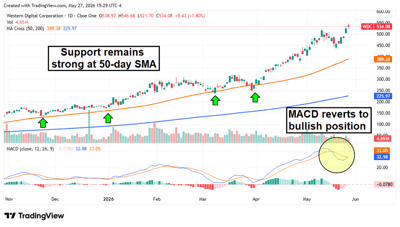

Several technical factors underpin the lengthy rally in WDC shares. The stock has strong support at the 50-day moving average, which has remained above the 200-day moving average for more than a year. A bearish crossover in the Moving Average Convergence Divergence (MACD) indicator briefly paused the rally, but a bullish reversal now appears to be underway as the stock makes new all-time highs.

Rambus: Undervalued Logic Company Licensing Necessary IP to Data Centers

Rambus is a classic “picks and shovels” play on the memory storage theme.

The company develops memory-interface systems that enable the GPU and memory stack to communicate within the data center mainframe, and it licenses them as IP.

High-margin licensing products that can be sold regardless of which memory company wins the design provide a steady, recurring revenue stream.

Additionally, the firm’s HBM4E Memory Controller, launched in April, is now the industry's fastest. The stock has surged more than 60% YTD but remains undervalued relative to peers in the AI space.

RMBS shares have been more volatile than WDC, but volatility is often the price investors pay for higher upside. The stock spent two months stuck in neutral, bouncing between the 50-day and 200-day moving averages as the Relative Strength Index (RSI) remained in bearish territory.

However, an April rally pushed the price above the 50-day moving average, and momentum improved when the RSI moved above 50 into bullish territory. The 50-day moving average now appears to be support, which bodes well for future upside potential.

onsemi: Sympathy Rally Without the Substance

onsemi also rallied 9% on the day of the Micron report, but the UBS thesis doesn’t really apply here.

The company traditionally makes chips for the automotive and industrial markets, which are cyclical and not closely tied to the broader AI space.

onsemi has some data center business, but it accounts for only a small portion of the company’s total revenue. For example, the $797 million in Q1 automotive revenue was more than half of the company’s total Q1 2026 sales.

Management expects data center revenue to double YOY in 2026, but that would still amount to just $500 million out of a projected revenue base of more than $6 billion.

While the company has a compelling bull thesis of its own, it remains outside the Micron paradigm. And an almost 90% gain over the last three months has the stock looking frothy. The price is now well above trend, and the MACD is hinting that the bullish upswing is losing momentum. It might be a good time to take profits on ON shares.

This email message is a sponsored email from Chaikin Analytics, a third-party advertiser of The Early Bird and MarketBeat.

This ad is sent on behalf of Chaikin Analytics, 201 King Of Prussia Rd., Suite 650, Radnor, PA 19087. If you would like to optout from receiving offers from Chaikin Analytics please click here.

If you need help with your subscription, please feel free to email MarketBeat's South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from The Early Bird, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC.

345 N Reid Pl. #620, Sioux Falls, South Dakota 57103-7078. United States..