Dear Friend,

Musk needed batteries. He built the Gigafactory.

Needed solar. Acquired SolarCity.

Needed data. Bought Twitter.

The pattern is clear: when a supplier becomes mission-critical, Musk doesn't negotiate. He acquires.

Right now, the most critical supplier in his $1.75 trillion empire is a small power infrastructure company — the one building the equipment Colossus literally can't run without.

For Musk, acquiring it would be pocket change.

For investors who own it before that happens, it could be life-changing.

Dylan Jovine has the name and ticker.

See the stock Musk's playbook says he needs >>

"The Buck Stops Here,"

Kelly Maguire

Behind the Markets

3 Stocks Rallying on Micron's Price Boost: Substance or Hype?

Submitted by Dan Schmidt. Publication Date: 5/28/2026.

Key Points

- UBS raised its Micron price target to $1,625 on May 26, citing long-term AI hyperscaler agreements and a concentrated three-company HBM supply chain.

- Western Digital and Rambus rallied in sympathy with Micron and appear fundamentally supported by similar data center demand and supply dynamics.

- onsemi's 9% sympathy rally looks unwarranted, as automotive chips dominate its revenue and the stock appears technically overextended after an 80% three-month gain.

- Special Report: Elon Musk’s $1 Quadrillion AI IPO

The raging semiconductor rally got another boost this week when UBS analyst Timothy Arcuri raised his price target on Micron Technology Inc. (NASDAQ: MU) to a stunning $1,625, nearly triple his previous target.

The stock was trading below $800 at the time of the upgrade, so the new target implied upside of more than 100% and a company valuation of over $1.8 trillion.

ALERT: Drop these 5 stocks before the market opens tomorrow! (Ad)

The Wall Street Journal is already raising the alarm about a potential market crash, and Weiss Ratings research points to the first half of 2026 as a particularly rough stretch for certain holdings.

Some of America's most popular stocks could take serious damage as a radical market shift plays out. Analysts at Weiss Ratings have identified five names you may want to remove from your portfolio before this unfolds.

If any of these are in your portfolio, now is the time to review your positions.

See the 5 stocks to avoidMU shares rallied nearly 20% the following day, and the broader industry seemed to join in, as the iShares PHLX Semiconductor ETF (NASDAQ: SOXX) advanced 6%.

When the entire industry seems to rally every day, it's easy for weaker companies to get caught up in the wave and soar to new all-time highs. But it's also important to remember Warren Buffett's quote about what happens when the wave recedes: you find out who’s been swimming without proper attire.

Why UBS Boosted Its MU Price Target by 200%

Arcuri’s May 26 price target increase reflected his view that high-bandwidth memory (HBM) is undergoing a fundamental shift from a cyclical semiconductor business to one driven by long-term AI infrastructure demand.

Instead of a cyclical manufacturing industry, HBM now has structural growth tailwinds led by two key factors:

Long-term Revenue Visibility: AI hyperscalers are running into HBM backlogs and are more willing to lock in long-term agreements for supply and access to next-gen products. Micron already has agreements in place for its entire 2026 HBM supply.

Concentrated Supply Chain: Producing HBM products at large scale is a capability currently possessed by only three companies: Micron, Samsung Electronics Ltd. (OTCMKTS: SSNLF), and SK Hynix. In its Q1 2026 earnings report, Micron projected that data center demand for HBM will exceed $100 billion by 2028, more than three times the $35 billion in HBM sales to data centers in 2025.

Given these secure, long-term agreements and the tight supply concentration, Arcuri argues that MU shares deserve a valuation similar to NVIDIA Corp. (NASDAQ: NVDA). However, the stock traded at under 10x forward earnings at the time of the call—far cheaper than the NASDAQ 100 average of 24x earnings, which helps explain the massive re-rating.

3 Stocks Rallying in Sympathy: Hype or Substance?

Many tech stocks in the AI and semiconductor space rallied sharply in sympathy, especially Western Digital Corp (NASDAQ: WDC), Rambus Inc. (NASDAQ: RMBS), and onsemi (NASDAQ: ON). But are these gains warranted? Despite the industry's exuberance, each company still requires careful due diligence to separate substance from hype.

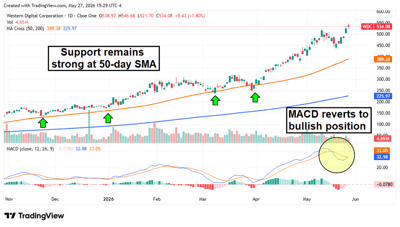

Western Digital: A Clean Complement to Micron’s Surge

Western Digital Corp. also rallied 8% on the day of the report, bringing its total year-to-date (YTD) gain to more than 200%.

Western Digital is now a pure hard disk drive (HDD) manufacturer following the SanDisk spinoff, and the same logic UBS applied to Micron’s HBM products also applies to Western Digital’s HDDs.

Hyperscalers are locking in long-term agreements, and the company’s production capacity through 2026 has already been claimed. The fiscal Q3 2026 earnings report on April 30 confirmed the bull thesis with a strong double beat, including 45% year-over-year (YOY) revenue growth and gross margins above 50%.

Several technical factors underpin WDC’s lengthy rally. The stock has strong support at the 50-day moving average, which has remained above the 200-day moving average for more than a year. A bearish crossover in the Moving Average Convergence Divergence (MACD) indicator briefly paused the rally, but a bullish reversal now appears to be underway as the stock makes new all-time highs.

Rambus: An Undervalued Logic Company Licensing Essential IP to Data Centers

Rambus is a classic “picks and shovels” play on the memory storage theme.

The company develops memory-interface systems that enable the GPU and memory stack to communicate within the data center mainframe, and it licenses them as IP.

High-margin licensing products that can be sold regardless of which memory company wins the design provide a steady, recurring revenue stream.

Additionally, the firm’s HBM4E Memory Controller, launched in April, is now the industry's fastest. The stock has surged more than 60% YTD but remains undervalued relative to peers in the AI space.

RMBS shares have been more volatile than WDC, but volatility is often the price investors pay for higher upside. The stock spent two months stuck in neutral, bouncing between the 50-day and 200-day moving averages as the Relative Strength Index (RSI) remained in bearish territory.

However, an April rally pushed the price above the 50-day moving average, and momentum improved when the RSI crossed above 50 into bullish territory. The 50-day moving average now appears to be support, which bodes well for future upside potential.

onsemi: Sympathy Rally Without the Substance

onsemi also rallied 9% on the day of the Micron report, but the UBS thesis doesn’t really apply here.

The company traditionally makes chips for the automotive and industrial markets, which are cyclical and not closely tied to the broader AI space.

onsemi has some data center business, but it accounts for only a small portion of the company’s total revenue. For example, the $797 million in Q1 automotive revenue was more than half of the company’s total Q1 2026 sales.

Management expects data center revenue to double YOY in 2026, but that still amounts to just $500 million out of a projected revenue base of more than $6 billion.

While the company has a compelling bull thesis of its own, it remains outside the Micron paradigm. And an almost 90% gain over the last three months has the stock looking frothy. The price is now well above trend, and the MACD is hinting that the bullish upswing is losing momentum. It might be a good time to take profits on ON shares.

5 Best Growth Stocks for the Next 10 Years

Submitted by Chris Markoch. Publication Date: 5/31/2026.

Key Points

- These 5 growth stocks are positioned to benefit from long-term megatrends, including AI, cybersecurity, fintech, and obesity treatments.

- Taiwan Semiconductor, Broadcom, and Cloudflare offer investors exposure to the growth of critical AI and internet infrastructure.

- Novo Nordisk and MercadoLibre combine strong competitive advantages with massive global market opportunities over the next decade.

- Special Report: Elon Musk’s $1 Quadrillion AI IPO

Picking growth stocks for a 10-year horizon is a different exercise than chasing this quarter's momentum. The goal is to identify companies with durable competitive advantages, exposure to structural megatrends, and enough financial strength to weather whatever the economy throws at them over that period.

Apple Inc. (NASDAQ: AAPL) is a good example of a growth stock that delivered a phenomenal, innovation-fueled run. That stretch has lasted more than 10 years and has turned AAPL into a forever stock in some portfolios. Here are five names that may be on a similar trajectory.

The Semiconductor Giant Powering the AI Boom

The #1 stock to buy BEFORE the June 12th filing (Ad)

When the SpaceX IPO launches, most retail investors will be locked out. The banks, funds, and insiders get in early - while everyone else waits on the sidelines.

But one small infrastructure supplier - a critical piece Musk can't scale the Colossus network without - is still trading well under institutional radar. A new briefing reveals the name and ticker at no cost.

Get the SpaceX infrastructure stock name and ticker hereIf there is one company that is structurally indispensable to the next decade of technology, it is Taiwan Semiconductor Manufacturing (NYSE: TSM). The Taiwanese chipmaker manufactures semiconductors for virtually every major chip designer worldwide and controls roughly 72% of the global foundry market.

TSM doesn't compete with its customers; it makes their chips. That means it wins regardless of which AI accelerator architecture prevails, which smartphone platform dominates, or which cloud provider gains share.

The AI infrastructure buildout has already lit a fire under Taiwan Semi's financials. Revenue grew 25% in 2025, and management is guiding for nearly 30% growth in 2026, backed by surging demand for its most advanced 3nm and 2nm manufacturing nodes. Hyperscalers are signing long-term agreements to lock in capacity.

Over the last 10 years, TSM has delivered a total return of more than 2,000%. That includes reinvested dividends, which now amount to an annual payout of $2.97 per share.

The company has increased that dividend by an average of more than 12% over the last five years.

The geopolitical risk around Taiwan is real and worth monitoring, but TSMC has responded by expanding manufacturing in the United States and Japan, diversifying its footprint to reduce that exposure. For investors who want broad AI exposure without picking winners in a fast-moving competitive landscape, TSM is about as close to a sure bet as the sector offers.

The AI Infrastructure Leader Benefiting From Custom Chips

Broadcom (NASDAQ: AVGO) tends to get lumped in with the broader semiconductor sector, but its story is more nuanced and arguably more durable than most chip stocks. The company operates two parallel businesses: custom AI silicon (ASICs) and infrastructure software.

Both are growing. AI revenue surged 106% year over year in the most recent quarter, and the company reported 29% total revenue growth. Analysts project its AI semiconductor revenue run rate could reach $100 billion by 2027.

The ASIC angle is what separates Broadcom from the pack. While NVIDIA dominates the GPU market, hyperscalers including Google, Meta, and Amazon are increasingly designing their own custom chips to optimize specific AI workloads. Those companies are turning to Broadcom to help build them.

Broadcom has deep, multiyear relationships with these customers and expertise in networking silicon that is extremely difficult to replicate. Add in sticky recurring revenue from its software businesses, including VMware products acquired in 2023, and you have a company generating exceptional cash flow with multiple durable growth engines.

AVGO is up more than 3,000% over the last 10 years, but the lion's share of that growth has occurred in the last three years. Broadcom is not cheap, and like TSM, it pays only a modest dividend, but for a 10-year holding period, investors are paying for a business that compounds reliably.

The Healthcare Growth Story Driving the GLP-1 Revolution

The GLP-1 revolution in metabolic health is not a fad. Obesity affects more than a billion people globally, and drugs like Wegovy and Ozempic have demonstrated efficacy well beyond weight loss—including cardiovascular and kidney benefits—that make them among the most consequential pharmaceutical advances in a generation. Novo Nordisk (NYSE: NVO) and Eli Lilly & Co. (NYSE: LLY) are the undisputed leaders in this space, with manufacturing scale and clinical pipelines that competitors will take years to match.

However, while LLY carries a lofty valuation, the market’s broad skepticism of NVO makes the stock more compelling on valuation grounds. Shares have pulled back meaningfully from their 2024 peaks as investors digested concerns about competition and questions about the company’s pipeline of oral formulations.

The result is that Novo now trades at just 11X earnings—a remarkable multiple for a company with this growth profile. The oral form of Wegovy is now available, driving sales growth and significantly expanding the addressable market. Meanwhile, the cash flows from the GLP-1 franchise are funding the development of entirely new therapy categories. A decade from now, Novo Nordisk's drug portfolio will likely look very different—and likely much larger—than it does today.

The Cybersecurity Platform Built for the Modern Internet

Cybersecurity is one of the few sectors where demand is structurally guaranteed to grow. As enterprises move workloads to the cloud, proliferate devices at the edge, and face increasingly sophisticated threat actors, the attack surface expands. Cloudflare Inc. (NYSE: NET) sits at an unusual intersection of cybersecurity, networking, and performance.

What distinguishes Cloudflare from other security vendors is its network architecture. Its global infrastructure spans more than 330 cities, enabling it to provide zero-trust security, DDoS protection, and application performance from a single integrated platform. Customers don't have to stitch together products from multiple vendors.

That integration is a powerful retention driver and creates significant cross-selling opportunities as Cloudflare continues expanding its product surface. Revenue has compounded at high rates for years, the company is approaching consistent profitability, and its total addressable market expands every time a new threat vector emerges. It is one of the few cybersecurity companies with a credible path to becoming the dominant security platform for the modern internet.

The E-Commerce and Fintech Leader Dominating Latin America

MercadoLibre Inc. (NASDAQ: MELI) is a company many U.S. investors know they should own more of but never get around to buying. The company is the dominant e-commerce and fintech platform across Latin America. It operates in a region with 650 million people, a growing middle class, underpenetrated digital commerce, and a financial system where large portions of the population remain unbanked.

The fintech layer—Mercado Pago—is now growing as fast as the commerce business and may ultimately be the more valuable of the two. Millions of Latin American consumers are using Mercado Pago as their primary financial account, building credit histories and accessing loans through MercadoLibre's platform.

The company has pricing power, network effects, and a logistics infrastructure that it has spent years building from scratch. Unlike many emerging-market plays, MercadoLibre has demonstrated consistent execution across multiple economic cycles in countries that are notoriously difficult to operate in. With decades of growth runway ahead, this is precisely the kind of business that rewards patient, long-term investors.

This email communication is a sponsored email from Behind the Markets, a third-party advertiser of InsiderTrades.com and MarketBeat.

If you need assistance with your account, please don't hesitate to contact our U.S. based support team at contact@marketbeat.com.

If you no longer wish to receive email from InsiderTrades.com, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 North Reid Place #620, Sioux Falls, SD 57103. United States..