Here’s what most investors won’t admit — the smartest money on Wall Street is already preparing for impact.

Look around:

– Gold just broke another record — a classic flight-to-safety signal.

– The NASDAQ is pricing in fantasy, not fundamentals.

– Global tensions are accelerating, not easing.

You won’t get an alert when the market collapses. It will happen overnight — and by morning, millions will be too late.

If you’ve been waiting for a sign to protect your portfolio…this is it.

Our research team just released a free crash-protection guide showing exactly which stocks and sectors can hold strong — even when the rest of the market crumbles.

👉 Download the Free Crash Protection Guide Now

(**By clicking this link you agree to receive emails from StockEarnings and our affiliates. You can opt out at any time. Privacy Policy. **)

Don’t be the investor who waits for confirmation.

3 Stocks Rallying on Micron's Price Boost: Substance or Hype?

Written by Dan Schmidt. Originally Published: 5/28/2026.

Key Points

- UBS raised its Micron price target to $1,625 on May 26, citing long-term AI hyperscaler agreements and a concentrated three-company HBM supply chain.

- Western Digital and Rambus rallied in sympathy with Micron and appear fundamentally supported by similar data center demand and supply dynamics.

- onsemi's 9% sympathy rally looks unwarranted, as automotive chips dominate its revenue and the stock appears technically overextended after an 80% three-month gain.

- Special Report: Have $500? Invest in Elon’s AI Masterplan

The semiconductor rally got another boost this week after UBS analyst Timothy Arcuri raised his price target on Micron Technology Inc. (NASDAQ: MU) to a stunning $1,625, nearly triple his previous target.

With the stock trading below $800 at the time of the upgrade, the new target implied upside of more than 100% and a company valuation of over $1.8 trillion.

Goldman Sachs just told you what to buy (most people missed it) (Ad)

Goldman Sachs just revealed that 40% of AI data centers will be crippled by electricity shortages by 2027 - not chips, not funding, but power. Demand is growing 15% per year and the grid can't keep up.

One small company makes the exact equipment these data centers need. They're sitting on $1.5 billion in orders, their hardware is already inside Musk's Colossus, and the stock still trades like a name nobody's heard of. Analyst Dylan Jovine is releasing the ticker for free.

See the stock positioned to solve AI's biggest power crisisMU shares rallied nearly 20% the following day, and the broader industry seemed to join in, as the iShares PHLX Semiconductor ETF (NASDAQ: SOXX) surged 6%.

When the entire industry seems to rally every day, it's easy for companies with weak fundamentals to get swept up in the wave and soar to new all-time highs. But it's also important to remember Warren Buffett's warning about what happens when the tide recedes: you find out who’s been swimming without proper attire.

Why UBS Boosted Its MU Price Target by 200%

Arcuri’s May 26 increase in Micron’s price target reflected his view that high-bandwidth memory (HBM) is undergoing a fundamental shift from a cyclical semiconductor business to one driven by long-term AI infrastructure demand.

Instead of a cyclical manufacturing industry, HBM now has structural growth tailwinds led by two key factors:

Long-term Revenue Visibility: AI hyperscalers are running into HBM backlogs and are increasingly willing to lock in long-term supply agreements for next-generation products. Micron already has agreements in place for its entire 2026 HBM supply.

Concentrated Supply Chain: Producing HBM products at scale is a capability currently held by only three companies: Micron, Samsung Electronics Ltd. (OTCMKTS: SSNLF), and SK Hynix. In its Q1 2026 earnings report, Micron projected that data center demand for HBM will exceed $100 billion by 2028, more than three times the $35 billion in HBM sales to data centers in 2025.

Given these long-term agreements and the heavy concentration of supply, Arcuri argues that MU shares deserve a valuation similar to NVIDIA Corp. (NASDAQ: NVDA). However, the stock traded at less than 10x forward earnings at the time of the call—far below the NASDAQ 100 average of 24x earnings, which helps explain the massive re-rating.

3 Stocks Rallying in Sympathy: Hype or Substance?

Many tech stocks in the AI and semiconductor space rallied sharply in sympathy, especially Western Digital Corp. (NASDAQ: WDC), Rambus Inc. (NASDAQ: RMBS), and onsemi (NASDAQ: ON). But are those gains warranted? Despite the industry’s exuberance, each company still deserves careful due diligence to separate substance from hype.

Western Digital: A Clean Complement to Micron’s Surge

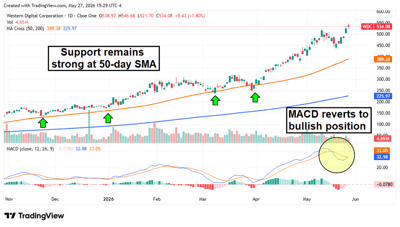

Western Digital also rallied 8% on the day of the report, bringing its total year-to-date (YTD) gain to more than 200%.

Western Digital is now a pure hard disk drive (HDD) manufacturer following the SanDisk spinoff, and the same logic UBS applied to Micron’s HBM products also applies to Western Digital’s HDDs.

Hyperscalers are locking in long-term agreements, and the company’s production capacity through 2026 has already been claimed. The fiscal Q3 2026 earnings report on April 30 confirmed the bull case with a strong double beat, including 45% year-over-year (YOY) revenue growth and gross margins above 50%.

Several technical factors underpin WDC’s extended rally. The stock has strong support at its 50-day moving average, which has remained above the 200-day moving average for more than a year. A bearish crossover in the Moving Average Convergence Divergence (MACD) indicator briefly paused the rally, but a bullish reversal now appears to be underway as the stock makes new all-time highs.

Rambus: Undervalued Logic Company Licensing Essential IP to Data Centers

Rambus is a classic “picks and shovels” play on the memory storage theme.

The company develops memory-interface systems that allow the GPU and memory stack to communicate within the data center mainframe, and it licenses them as IP.

High-margin licensing products that can be sold regardless of which memory company wins the design create a steady, recurring revenue stream.

Additionally, the firm’s HBM4E Memory Controller, launched in April, is now the industry’s fastest. The stock has surged more than 60% YTD but remains undervalued relative to peers in the AI space.

RMBS shares have been more volatile than WDC, but volatility is often the price investors pay for greater upside. The stock spent two months stuck in neutral, bouncing between the 50-day and 200-day moving averages as the Relative Strength Index (RSI) remained in bearish territory.

However, an April rally pushed the price above the 50-day moving average, and momentum improved when the RSI crossed above 50 into bullish territory. The 50-day moving average now appears to be acting as support, which bodes well for future upside potential.

onsemi: Sympathy Rally Without the Substance

onsemi also rallied 9% on the day of the Micron report, but UBS’s thesis doesn’t really apply here.

The company traditionally makes chips for the automotive and industrial markets, which are cyclical and not closely tied to the broader AI space.

onsemi has some data center business, but it accounts for only a small portion of the company’s total revenue. For example, the $797 million in Q1 automotive revenue was more than half of the company’s total Q1 2026 sales.

Management expects data center revenue to double YOY in 2026, but that would still amount to just $500 million out of a projected revenue base of more than $6 billion.

While the company has a compelling bull case of its own, it remains outside the Micron paradigm. And an almost 90% gain over the last three months has the stock looking frothy. The price is now well above trend, and the MACD is hinting that the bullish upswing is losing momentum. It may be a good time to take profits in ON shares.

Burlington Beat Earnings Estimates, But Not Investor Expectations

Submitted by Jennifer Ryan Woods. Article Published: 6/1/2026.

Key Points

- Burlington Stores reported adjusted EPS of $2.01, a 26% increase year over year, marking its 14th consecutive quarter of double-digit earnings growth.

- Despite beating estimates and raising full-year guidance, BURL shares initially fell nearly 8% after the report, reflecting elevated investor expectations.

- Burlington's post-earnings decline contrasted with peers TJX and Ross Stores, whose shares rose more than 5% and 8%, respectively, after their own strong results.

- Special Report: Have $500? Invest in Elon’s AI Masterplan

Burlington Stores Inc. (NYSE: BURL) delivered another better-than-expected quarter on May 28, marking its 14th consecutive quarter of double-digit earnings growth.

The company also raised its full-year outlook as off-price retailers continue to benefit from demand from budget-conscious consumers seeking bargains. Still, that wasn't enough to satisfy investors, as shares fell sharply following the report.

Burlington Earnings Beat Expectations

The #1 stock to buy BEFORE the June 12th filing (Ad)

When the SpaceX IPO launches, most retail investors will be locked out. The banks, funds, and insiders get in early - while everyone else waits on the sidelines.

But one small infrastructure supplier - a critical piece Musk can't scale the Colossus network without - is still trading well under institutional radar. A new briefing reveals the name and ticker at no cost.

Get the SpaceX infrastructure stock name and ticker hereFor the quarter, the company reported adjusted earnings per share (EPS) of $2.01, up 26% from year-ago earnings of $1.60 and well above Wall Street’s expectations of $1.77 per share. Revenue rose 14% year over year (YOY) to $2.86 billion, topping analyst estimates by more than $57 million.

Comparable-store (comp) sales increased 6% YOY, above the company’s guided range of 2% to 4%, while gross margin expanded 30 basis points to 44.1% of net sales.

On the earnings call, Chief Executive Michael O’Sullivan said, “These results add to an already very impressive track record of consistently converting sales growth into strong margin expansion and earnings flow-through.”

Burlington Raises Full-Year Guidance on Strong Off-Price Demand

The company also issued second-quarter guidance and raised its full-year sales and earnings outlook. For Q2, Burlington expects comp sales growth of 1% to 3%, with total sales increasing 10% to 12%. Operating margin is expected to expand 30 to 60 basis points YOY, while adjusted EPS is forecast to be between $2.05 and $2.20.

For the full year, Burlington now expects comp sales growth of 2% to 4%, up from prior guidance of 1% to 3%. Total sales are expected to rise 9% to 11%, up from the prior outlook of 8% to 10%, while adjusted EPS is projected to range from $11.45 to $11.80, above the previous forecast of $10.95 to $11.45. The company also said it now expects net new store openings of 115, up from 110.

O’Sullivan also discussed how higher oil prices and the conflict in the Middle East have influenced the company’s outlook since the previous earnings call. Burlington remains optimistic about the second half of the year, though management is taking a more cautious view than it did in March because of higher gas prices and the potential impact on inflation.

Even so, O’Sullivan said a tougher consumer backdrop could work in Burlington’s favor if shoppers become more focused on value. "In fact, as a value retailer, it could turn into an opportunity," he said.

Shares Tumble Despite Strong Quarter and Better Outlook

Burlington may have cleared Wall Street’s estimates, but not necessarily the market’s expectations. After the report, BURL stock initially fell nearly 8%, trading near $300, before recovering much of that decline in subsequent trading.

Ahead of the earnings release, the stock had been on a major multiyear run. After normalizing from pandemic-era highs, Burlington shares were trading around $110 in September 2022. Since then, the stock has surged roughly 175%, including a gain of more than 25% over the past year, leaving investors with a higher bar for another beat-and-raise quarter.

The post-earnings sell-off comes shortly after Burlington shares hit a 52-week high above $351 in April, potentially signaling some profit-taking following the stock’s multiyear run. It may also indicate that investors were looking for stronger comp sales growth and a more robust outlook for comparable-store sales.

During the earnings call, one analyst questioned whether Burlington’s focus on earnings may have caused it to miss opportunities to drive additional comp growth in Q1. In response, O’Sullivan said, “I do think that we may have an opportunity to loosen our belts a notch and get slightly more aggressive on sales.”

Burlington Sell-Off Contrasts With Off-Price Peers

The reaction to Burlington’s earnings was very different from some of its off-price peers, whose shares moved higher following their own better-than-expected earnings reports.

Shares of TJX Companies Inc. (NYSE: TJX) rose more than 5% after the company's recent earnings and revenue beats on May 20, while Ross Stores Inc. (NASDAQ: ROST) gained more than 8% two days later following its strong Q1 report.

In terms of valuation, the three stocks have similar price-to-earnings (P/E) ratios, with Burlington trading around 34x earnings, TJX at 30x, and Ross Stores at roughly 32x. The broader retail industry is trading at an average P/E ratio of 25x.

Despite Burlington’s post-earnings decline, Wall Street analysts remain largely bullish on the stock.

Ahead of the report, the average 12-month price target stood around $357, implying more than 18% upside from current levels.

The stock currently carries a Moderate Buy consensus rating, based on 16 Buy ratings and five Hold ratings. The $351 analyst consensus price target implies about an 8% potential upside.

While Burlington’s latest quarter highlighted the continued strength of the off-price sector, the market reaction suggests investors may have been hoping for more signs of strength in comparable-store sales.

Still, with consumers remaining focused on value amid economic uncertainty, Burlington could be well-positioned if bargain hunting continues to drive retail spending.

This email content is a paid sponsorship for StockEarnings, a third-party advertiser of DividendStocks.com and MarketBeat.

If you have questions about your subscription, please contact MarketBeat's South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from DividendStocks.com, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 N Reid Pl., Sixth Floor, Sioux Falls, S.D. 57103-7078. U.S.A..